Are you looking for a vehicle but don't have the equity? In Switzerland, you can benefit from various types of financing.

- Leasing

- "Car finance"

- Personal credit

We'll compare these options to determine which financing is best suited to your needs.

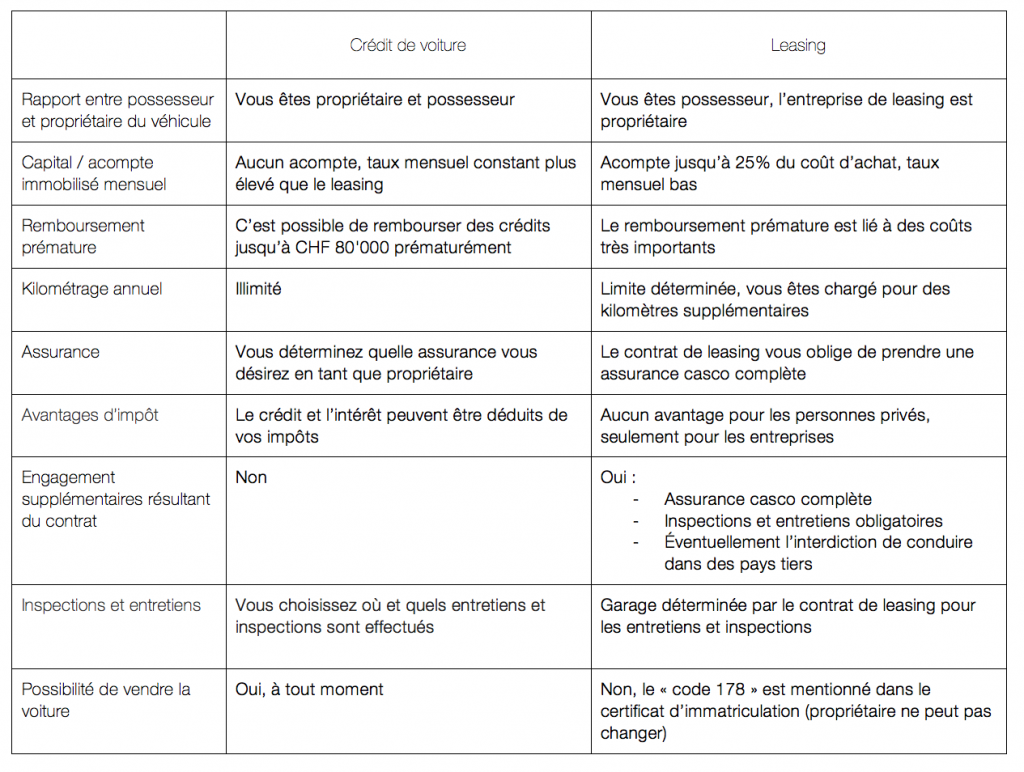

Leasing:

Although the interest rates of a lease may seem more attractive, especially on new cars where interest rates of 0.9% are sometimes offered, it is an option with many disadvantages and hidden costs:

- First of all, you have to advance an amount equivalent to a monthly lease payment, which means that in the 1st month, you will have to pay twice the monthly payment.

- Secondly, and one of the biggest drawbacks, you are a user but not an owner. The vehicle does not belong to you for the entire period of reimbursement, and even afterwards. If you want to own the vehicle at the end of the lease, you will have to pay a sum called residual value. This amount is agreed upon when the leasing contract is signed. The lower the residual value, the higher the monthly payment on your lease.

- Third, unlike a loan, you can't deduct a lease from your taxes. Indeed, the vehicle (and the lease) do not technically belong to you, they belong to the financing company (AMAG, RCI, FCA, BMW leasing, etc.). To find out how to get a tax deduction with a credit, click here.

As for the personal loan, it is in your name only, it is in the eyes of the administration, a personal debt whose interest is deductible from taxes, more precisely from your taxable income.

It is true that leasing is in itself a debt in the same way as credit, but in reality, you are leasing the vehicle.

- Finally, the mandatory additional fees:

- Obligation to take out comprehensive insurance covering damage caused to the vehicle by you and others. This insurance costs about a hundred francs per month.

- You will also be limited with an annual mileage, agreed upon when signing the contract, any additional mileage will be charged to you

- You will be charged for the final statement, whereas it is free with the credit

- Maintenance is mandatory and usually has to be carried out in partner garages, so you won't necessarily have a choice of garage.

Car Finance

Car finance, like a personal loan, allows you to immediately own the vehicle you are looking for.

You will therefore be able to sell the vehicle when needed, unlike leasing. There are also many other significant advantages:

- The annual interest will be tax deductible. For example, if you have 500 francs in interest over a year, you can deduct this amount from your taxable income.

- The interest rate is equivalent to that of leasing. Since the finance company giving you a loan with a guarantee on an asset, in this case the vehicle, interest rates that are more or less similar to leasing can be granted.

- No refund limit. You only have to pay the agreed minimum monthly instalment, but if you wish, for example, to pay 3 (or more) monthly instalments at once, you are free to do so. This will have the advantage of lowering the total interest on your loan. The sooner you pay, the less interest you'll have in total.

- No mileage limit. No unpleasant surprises at the end of the refund, you won't end up with thousands of extra francs to pay for the extra kilometres you have driven. The vehicle is yours, so you can do whatever you want with it!

- No deposit to advance. Unlike leasing, you don't have to pay any money up front when signing the contract.

- No residual value. You don't have to pay anything at the end of the refund.

- Choose the car insurance coverage of your choice.

- No service obligations. Perform your service wherever and whenever you want.

To find out more about the specifics of the residual value, we invite you to click on this link.

Personal credit:

Personal credit is an option that is almost identical to car finance. The only difference is that with a personal loan, you don't have to put the car as collateral for your loan.

On the other hand, car finance is not available for just any vehicle and the money will go through the garage in question to directly finance the vehicle of your choice

With a personal loan, you receive the money in your account, and you are free to do whatever you want with it.