What is a debt collection?

When you don't pay a bill, and the creditor can't get the money from you, they can then sue you.

This is the legal route to obtain the repayment of a debt. As a result, there will be a registration with a debt collection office, and it is the debt collection office that will take care of taking the steps to collect the amount owed.

A debt collection usually occurs after one or more recalls. It is said to be requisitioned by the creditor from the relevant debt collection office (i.e. the debt collection office corresponding to the area where the debtor is registered) using a debt collection requisition form.

To find out your debt collection situation, you must order your extract from the debt collection register online, or directly from the relevant office. We invite you to read this article to find out where and how to order your extract.

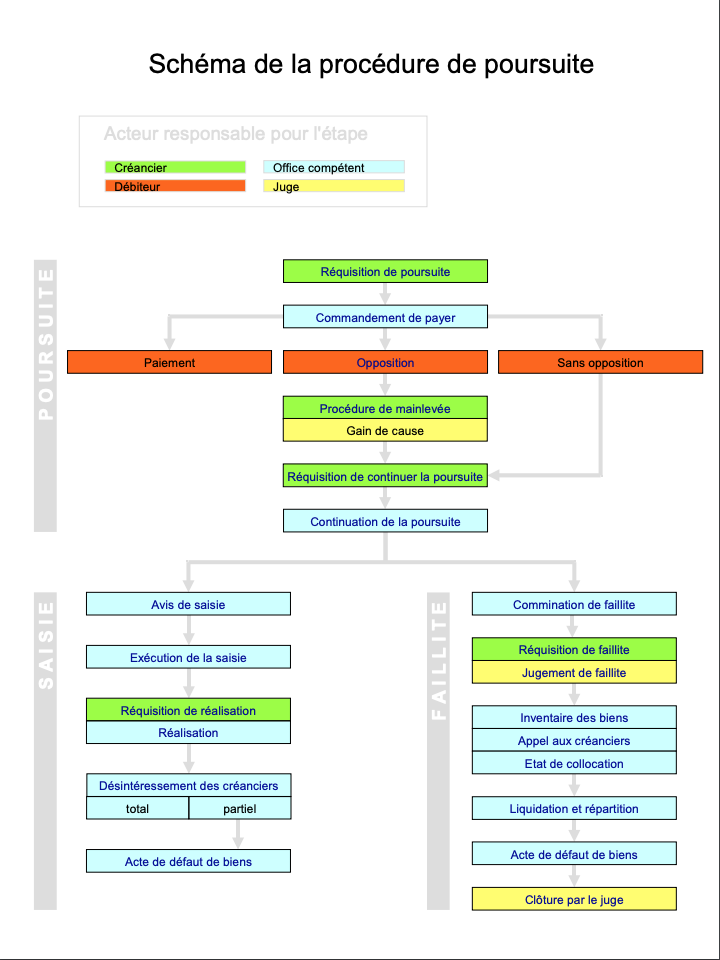

The Prosecution Procedure

The course of a debt collection always starts with the creditor's request to prosecute, you will then be sent a payment order where you will have 20 days to pay. If you do not do so within this period, the creditor will have to request a requisition to continue the debt collection and you will then be summoned to the debt collection office. At the time of this summons, a statement of your financial situation will be drawn up to determine whether or not you can be seized.

If you are seizable, your salary will be garnished. If you are not seizable, a certificate of default of property will be issued. Don't forget that the seizure can also involve movable property (car, jewelry, etc.) or real estate (apartment, house)

A certificate of default of assets remains registered in your debt collection register for 20 years and if you return to better fortune, the creditor will have the possibility to request the garnishment of your salary to settle these certificates of default of property.

You can also object to the debt collection within 10 days of notification of the order to pay. However, evidence must be provided that the lawsuit is unjustified for the objection to be admissible, otherwise the creditor may apply to a competent court for the withdrawal to be made.

Unwarranted prosecution?

In Switzerland, anyone can sue someone, without having to justify the authenticity of the debt collection.

If this happens to you, you will have to take steps to obtain the cancellation of the wrongful prosecution and make an advance of costs which amounts to a flat rate of Fr. 40.00 for your request to be admissible and studied.

How do I get out of the debt collection?

In Switzerland, it is more common than you think to end up in court. One of the main reasons is taxes, which, unlike a majority of countries, are not taxed at source. As a result, many people are unable to save money for their taxes and end up having to pay several thousand francs at the end of the year.

However, getting out of the spiral of over-indebtedness is not impossible, with the right support everyone can do it.

At Milenia, we have been working in the field of solvency since the early 2000s. We are the professional support you need to get out of debt. Here's what we offer you with debt restructuring:

- Stop your creditors' reminders

- Preventing debt collection and seizure

- Have a single affordable monthly payment to get out of debt

- Get your head out of the water and get back to a peaceful sleep

The benefits for you are numerous, but the main ones are:

- Your debts are stopped and your creditors' reminders stop

- You only have one person to talk to who never judges you

- You are free to stop at any time

- You don't create new debt

- Confidentiality and discretion guaranteed (we do not contact anyone other than your creditors)

How do I clear my debt collections ?

It is important to know that even after having paid your debt collection in full, it remains registered for 5 years (order to pay) or 20 years (certificate of default of property) if no action is taken.

Suffice to say that this will block you for many years in your efforts, such as looking for an apartment, obtaining a financial loan and even looking for a job. In addition, the debt collection extract is only one of the credit registers consulted in Switzerland in which you can be rated negatively.

We can analyse and clean your credit registers, do not hesitate to contact us on 021 620 60 00 or make your request directly on our website and our advisors will be happy to help you in your efforts.